December 22, 2009

The Deflation Threat

Contrary to what you are hearing in the media, the worst economic news may still lie ahead: A deflationary depression is descending upon us. Could it help the conservative movement?

Breakneck federal printing of debt and dollars, gold and stocks rising, the dollar falling -- surely these trends presage inflation, or even hyperinflation. So goes the narrative across the media. But a contrarian and increasingly likely view is that deflation, not inflation, awaits.* What is deflation? How will it develop? How will it affect us? And what does it mean for the Democrats' future?

Most of us have known only inflation, in which prices rise over time. In deflation, prices fall. The last time this happened in the U.S. was during the Great Depression. Japan has been living it these last fifteen years.

A falling price trend is at first a benefit to consumers. But then it leads to a spiral of economic decline: a depression. Deflation occurs when money for whatever reason becomes scarce, and therefore more valuable. Lower prices are the effect. Producers starve for profits, which leads to layoffs, loan defaults, and bankruptcies. Borrowers find they have to repay with more expensive dollars, so they pay off their debts. Low debt throttles growth and slows purchases. Expensive dollars make exports less competitive. Unsold inventories waste away on the shelf, crumble in value, and must be sold at deep discounts. Prices fall further, and so on, in a vicious circle.

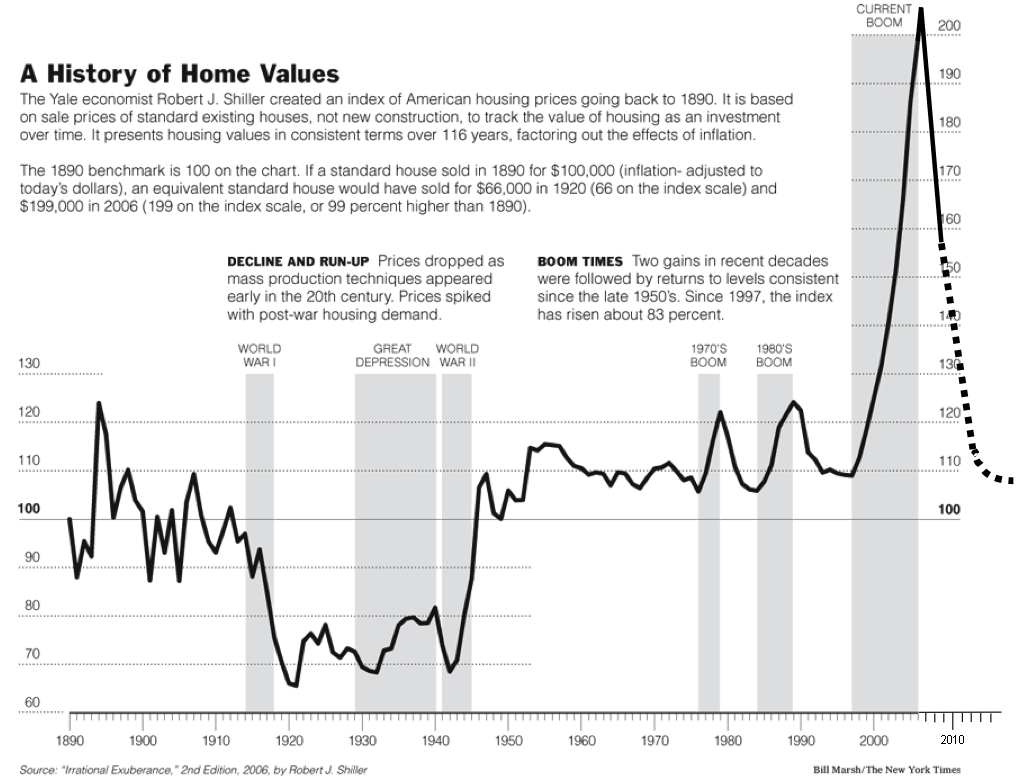

Normal downturns are triggered by cyclic imbalances in which supply temporarily exceeds demand. Growth pauses while inventory excesses are liquidated. This time, however, things are different. The triggering event was an asset valuation bubble -- high stock and real estate prices -- boosted excessively in a buying mania fueled by cheap credit during the last fifteen years. Lots of borrowing creates financial leverage, which pumps up profits during good times and wipes them out during bad. Consumer credit swelled with the aid of cheap mortgages and home equity lines. Businesses borrowed cheap short-term money and invested long-term, expecting to roll the loans over as profits expanded. Most significantly, bankers ran high ratios of what they lent out versus what they took in. All of this borrowing was encouraged by the Federal Reserve Board and Congress to foster social goals like full employment and high levels of homeownership.

But the system eventually became unstable. The real estate that served as collateral for trillions of dollars of debt on the banks' (and the bank-like Fannie and Freddie) balance sheets became priced too high, and for the first time in seventy years, prices began a serious decline. Many highly leveraged borrowers had their equity wiped out, so they threatened to default. An increased sense of risk rippled through these debt pools, erasing much of their value and rendering them unsalable, or "toxic." Soon, a "run," or loss of general confidence, pervaded the U.S. and European economies. Though it has come to be called the housing bubble recession, a better name is the great credit bubble depression.

Deflation stems from a shortage of money. Isn't the Fed creating trillions of new dollars that they lend to banks and to the Treasury for disbursement in "stimulus" programs? Yes, but even as the Fed has recently created $2 trillion in new assets, many times, more money has been and will continue to be taken out of the world's economy through the process of de-leveraging -- that is, the paying off or writing off of a portion of the hundreds of trillions in credit floated around the world. Despite talk of TARP success and nascent recovery, those toxic assets are still on the books, some with the banks and some with the Fed itself. Eventually, much of this money will become worthless. As fast as the Fed is printing new money, money is being destroyed as debt is taken off the table. In the end, the Fed will lose as the quicksand of depression sucks more and more money into its muck.

Ironically, the 60% stock market rally of 2009, which in itself is anti-deflationary, is no source of comfort. Though it's hard to prove why stocks move, the recent rally is most likely due to a "carry trade," in which banks borrow cheaply from the Fed and invest in high-return risk markets like stock, gold, or even foreign currencies. The Fed is encouraging this with low rates precisely because this asset re-inflation makes the dollar less valuable. They are fighting the inevitable deflation.

But they are also creating a new asset bubble just like the one that imploded last year. They have lowered short-term interest to zero. As prices correct downward and the dollar rises as deleveraging continues, the Fed can take rates no lower. The last remedy available is for the Fed to buy government and corporate debt in the open market, literally printing money at will -- adrenaline for a burst, perhaps, but not sustainable. Other government measures like deficit spending and expansion of primarily public sector jobs in the "Stimulus" program are simply wasteful, destroying more dollars in the present and creating public debt to burden the future. These effects are deflationary. Obama's plans for new taxes and regulations, which extinguish dollars, are also deflationary.

What about the oft-cited signs of recovery like upticks in GDP, consumer sentiment, and retail sales? Well, even in a trending economy -- and ours is trending down -- it is normal to see short blips, zigs, and zags against the trend. The numbers are also somewhat cooked for political effect. You'll know that the grip of deflation is tightening if you continue to see more of the following: discounts, price reductions, joblessness, real estate vacancies, bank failures, business failures, public finance failures, pension defaults, loan defaults, shrinking debt and credit, higher savings ratios, and frugal spending.

When Obama took office, conservatives grumbled that he would get an unearned lift in 2012 because the natural tendency of recessions to reverse themselves after two years would put the country on a positive trajectory just in time to lift him to a second term. The thing about deflationary depressions is their persistence. If Japan is a guide, we'll be seeing this one for a decade or more. Its ill effects should intensify within the 2010 election cycle. It will be far from over, even by 2012.

The depression will be terrible, but it could have a cleansing effect. We are already seeing the rejection of carbon taxation, for example, because of the hard times. The entire costly Democratic program to expand government against the deflationary backdrop will catch the public's anger and lead them to "throw the bums out."

Obama's economists, Larry Summers and Ben Bernanke, are smart enough to understand and see the lurking deflation, even if they publicly brag that the worst is over. They might even quietly suspect that their current policy mix will not stop deflation. So what have they told the boss? If they are speaking honestly, then Obama must already know how much pain is coming our way. Or are these generals cowering before their stern commander, who will shoot a messenger bringing unwelcome news? The mood must be pretty tense.

During the Iraq war, the Dems seemed to be rooting for military defeat as a tactic to win political victory. Their interests were contrary to the country's. This time, in contrast, conservatives want recovery -- a development in alignment with the public interest, but which could also boost Democrat prospects. What Republicans wish for matters not. If depression develops, it will not come from conservative's wishing, but at least they will have the cold dish of revenge at the polls to relish.

*While the forecast is deflation for the next few years, inflation is still a long-term threat. Economic trends swing to and fro. A mild deflation could be followed by a mild inflation. Unfortunately, we may see a very deep deflation change into a hyperinflation as panicky anti-deflationary policies overshoot their mark.

{kind=link}

FOLLOW US ON

Recent Articles

- Why Do Democrats Hate Women and Girls?

- There is No Politics Without an Enemy

- On the Importance of President Trump’s ‘Liberation Day’

- Let a Robot Do It

- I Am Woman

- Slaying the University Dragons

- Canada Embraces European Suicide

- A Multi-Point Attack on the National Debt

- Nearing the Final Battle Against the Deep State

- Now’s the Time to Buy a Nuke (Nuclear Power Plant, That Is)

Blog Posts

- Pete Hegseth in the line of fire—again

- Canadian Prime Minister Mark Carney is accused of plagiarizing parts of his Oxford thesis

- France goes the Full Maduro, bans leading opposition frontrunner, Marine Le Pen, from running for the presidency

- Bob Lighthizer’s case for tariffs

- An eye for an eye, an order for order

- Peace on the Dnieper?

- Tesla protestor banner: 'Burn a Tesla, save democracy'

- Pro-abortionists amplify an aborton protest's impact

- A broken system waiting to crash

- The U.S. Navy on the border

- Rep. Jasmine Crockett opens her mouth again

- Buried lede: San Francisco has lost 60,000 tourism-related jobs

- I’ve recognized manipulation in the past, and I see it now on the Supreme Court

- The progressive movement has led the Democrat party into a political black hole

- A Colorado Democrat’s immoral cost-benefit analysis to justify taxpayer-funded abortion